Updated June 2026

What Is Uninsured Motorist Coverage Insurance?

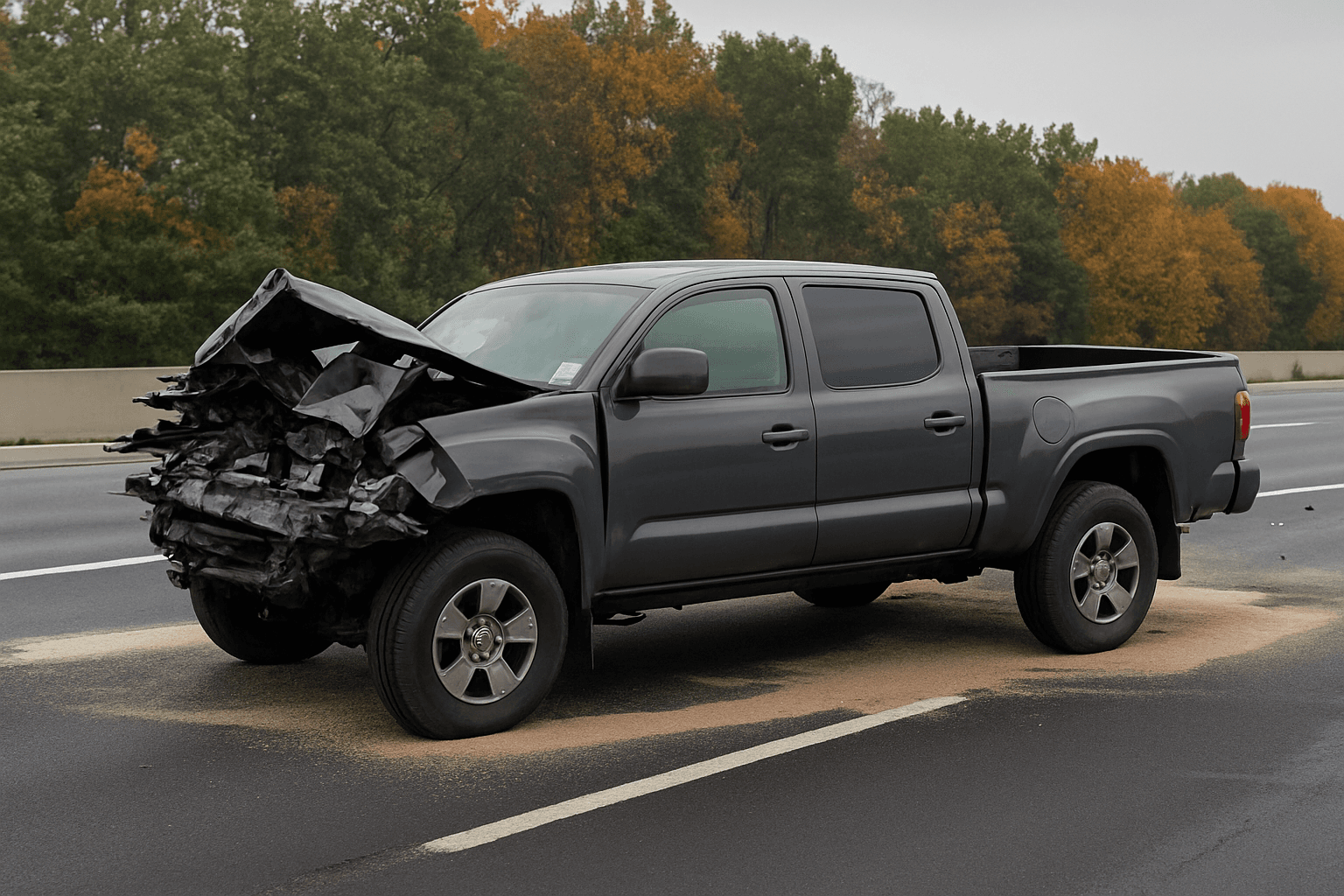

Uninsured Motorist Coverage steps in when the at-fault driver has no insurance or insufficient coverage to pay your medical expenses, lost income, and pain and suffering. It also covers hit-and-run crashes where the driver cannot be identified. This coverage follows your policy limits — if you carry $50,000 in UM coverage and have $60,000 in medical bills from an uninsured driver's mistake, you collect $50,000 from your own carrier and absorb the remaining $10,000 yourself unless you have health insurance to cover the gap.

- You're rear-ended at a stoplight by a driver with no insurance. You have $25,000 in medical bills and miss six weeks of work, losing $4,800 in wages. The at-fault driver has nothing to pay you. Your UM coverage pays the full $29,800 up to your policy limit. Without UM coverage, you pay those costs yourself or negotiate payment plans with hospitals while trying to sue a driver with no assets.

- A driver runs a red light, T-bones your car, and flees the scene. You suffer a broken collarbone and $18,000 in medical expenses. Police never identify the driver. Your UM coverage treats this as an uninsured motorist claim and pays your medical costs and lost income up to your limit. Without UM, you file through health insurance if you have it, or pay out of pocket.

- You're hit by a driver who carries Arizona's minimum $25,000 bodily injury limit. Your injuries require surgery, totaling $55,000. The at-fault driver's insurer pays their $25,000 limit. If you carry $50,000 in Underinsured Motorist coverage, your policy pays the remaining $30,000. If you don't have UM/UIM, you're responsible for that $30,000 gap yourself.

Who Needs Uninsured Motorist Coverage Insurance?

If you're reinstating your license after a suspension and need to maintain continuous coverage to avoid another suspension, UM coverage is critical. A crash with an uninsured driver creates medical bills you can't afford and a gap in coverage that triggers a new suspension if you drop your policy to avoid paying those bills. If you're carrying an SR-22 after a DUI or driving uninsured conviction, one uninsured driver hitting you can spiral into a financial crisis that keeps you suspended longer.

Compare the monthly UM premium to your health insurance deductible and out-of-pocket maximum. If your health plan has a $7,500 deductible and UM costs $12 per month, UM pays for itself in one serious crash. If you have no health coverage or a high-deductible plan, UM is not optional — 13% of Arizona drivers are uninsured, and you will eventually share the road with one.

How Much Does Uninsured Motorist Coverage Insurance Cost?

Uninsured Motorist Coverage typically adds $8–$18 per month or $96–$216 per year to an Arizona auto insurance policy, depending on the coverage limit you select and your driving history.

- Coverage limit selected — $25,000 UM costs less than $100,000 UM, but higher limits protect you better in serious crashes

- Your county's uninsured driver rate — Maricopa and Pima counties have higher uninsured rates, which can raise UM premiums slightly

- Stacked vs. non-stacked coverage — stacking multiplies your UM limit by the number of vehicles on your policy, increasing cost but also protection

- Your liability limits — carriers typically cap UM limits at or below your liability limits, so higher liability coverage can increase UM pricing options

- Claim history — prior UM claims can raise your premium, even though you weren't at fault, because you represent higher utilization risk to the carrier